Business

Business

The goal of the project is to develop and apply methods that will improve the ability of the hydrocarbon industry to improve capital efficiency.

Program

This project was selected as a small purchase to provide DOE with state-of-the-art information on Asset Risk Management in the petroleum industry.

University of Texas at Austin

Austin, TX

Chevron Producing Company

Houston, TX

Statoil

Stavanger, Norway

Devon Energy

Oklahoma City, OK

Pioneer Energy

Dallas, TX

Pecon Energia

Buenos Aires, Argentina

The primary incentives for the work are the following observations:

Project Results

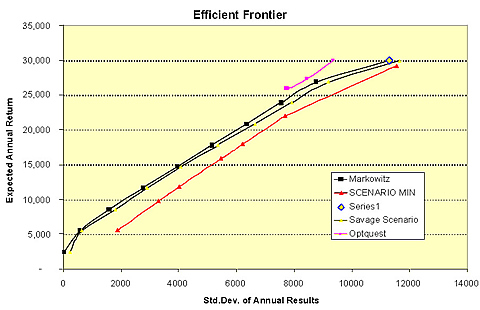

This ongoing project has revealed new ways to evaluate options in reserve estimation, in value of information, and in evaluating asset portfolios.

Benefits

Hydrocarbon evaluation has been done historically in a deterministic manner. That is, even though it is widely acknowledged that there are substantial uncertainties in prediction, decisions are made on the basis of fixed information. This work will show whether the operators' decision-making can be improved if this uncertainty is accounted for.

Project Summary

The project has two main objectives:

The project is ongoing. DOE supported the initial stages of the project. The current work is completely industry-supported.

Publications

The project does not require annual reports. The following are theses or dissertations that are completed or are nearing completion:

Hahn, Warren, Dyer, Jim, Incorporating Mean-Reverting Price Forecasts into Exploration and Production Valuation, April 2005.

Brandao, Luis, Dyer, Jim, Hahn, Warren, Using binomial decision trees to solve real option valuation problems, May 2005.

D'Addosio, Pierangaela, Analysis of risk cultures, August 2005

Portillo, Maria, Optimizing gas production under uncertainty, August 2005

Lawal, Azeez, A sensitivity analysis of the uncertainties of oil production, August 2005

Hultszch, Paul, Estimating the benefits of options in reserve estimation, December 2005

Faya, Luis, Using portfolio optimization for oil field assets, May 2006.

Min, Namhon, The value of oil field information, May 2007.

$95,000

$230,000 (67% of total)

NETL - Rhonda Jacobs (Rhonda.jacobs@netl.doe.gov or 918-699-2037)

UT, Austin - Larry W. Lake (Larry_Lake@mail.utexas.edu or 512-471-8233)